Skip to the content

Skip to the content

CONTACT ETS

If you have any questions or would like to discuss further what you should be doing, ETS is here and willing to help.

Call 0117 205 0542

Email enquiries@energy-ts.com

Submit a contact form

CHECK OUR SERVICES

Blog Summary

● Understand ESOS Phase 4 Requirements

● How Identify and Implement Energy-Saving Strategies

● Leverage Expert Support for Compliance

What is ESOS and Why Does it Matter?

ESOS was introduced by the UK government in 2014 to comply with European Legislation, tackle energy use, efficiency and rising carbon emissions, which necessitates comprehensive audits and customised measures to be completed in 4-year phases. These audits should identify cost-effective energy-saving opportunities in business operations, including buildings, industrial processes, and transportation, which improve the company’s energy management.

Phase 3 of ESOS placed a stronger emphasis on moving beyond audits to drive the actual implementation of identified energy-saving opportunities by enforcing organisation to produce and report on action planning and delivery. Acting on energy efficiency recommendations offers participants the chance to reduce energy consumption and costs while supporting the UK’s net zero commitment by cutting emissions.

WHO NEEDS TO COMPLY?

Energy audits play a crucial role in identifying opportunities to improve energy efficiency within an organisation. These audits involve a systematic review of energy consumption patterns, equipment performance, and operational processes. By analysing this data, ETS auditors can pinpoint inefficiencies and recommend tailored solutions to reduce energy usage, lower costs, and minimize environmental impact.

ETS follow the BS EN 16247 audit methodology. The process typically includes:

- Data Collection: Gathering information on energy usage, equipment specifications, and operational practices.

- Field Work: This entails a site inspection for a building audit, examining facilities to assess the performance of systems such as lighting, HVAC, and machinery. For transport, we will conduct an assessment in collaboration with personnel from the operations department and evaluate fleet to identify potential issues and opportunities for energy reduction.

- Analysis and Benchmarking: Comparing energy use against industry standards or similar operations to identify gaps.

- Recommendations: Providing actionable steps to improve efficiency, optimize systems, and reduce energy waste.

Common Areas for Savings

Typical sectors like lighting, refrigeration, HVAC (Heating, Ventilation and Airconditioning) systems, building fabric and insulation, and equipment efficiency, behaviour change, controls, energy monitoring and management, process improvements, low carbon technologies.

Case Study: ESOS audit for UK Retail Chain

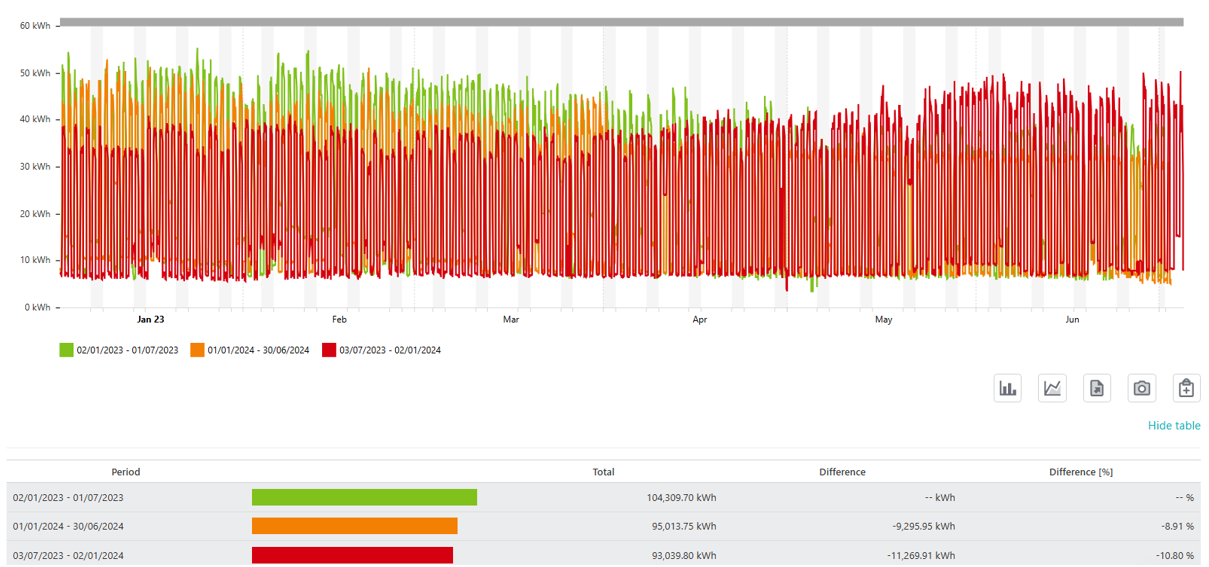

ETS caried undertook an ESOS audit on behalf of a retailer with a chain of DIY outlets throughout the UK. 180 sites formed the scoped of the assessment and 23 sites were selected as the survey sample. It was observed that lighting was left on when areas were unoccupied as a result of poor staff energy awareness and poorly managed lighting controls. Behaviour change and ‘switch off’ culture was recommended as a short term solution to energy savings with a longer term goal to install intelligent controls to remove manually and out of date systems.

kWh per annum projected – 21,030kWh

kWh achieved per annum – 22,539.82 kWh (11,269.91kWh for 6 months prorated)

Cost savings achieved – £7,461

CO2 projected savings – 4354kgco2e

CO2 Achieved savings – 4667kgco2e

The energy savings initiative is applicable to multiple stores yielding substantial benefits. Applying the same process to 10 stores is projected to achieve total savings of approximately £74.610.

Gas was used in the same store for low temperature hot water (LTHW) system which was running inefficiently and needed to be properly maintained. There was need to install a BMS with zoned temperature control as well as install additional Destratification Fans for heating efficiency. However, not all actions were feasible to implement. A year on year review of the gas use showed a 15% savings in the hot water system use.

Predicted savings kWh – 158509

Realised savings kWh – 23,580

Cost Savings – £1,627

The energy savings initiative is applicable to multiple stores yielding substantial benefits. Applying the same process to 10 stores is projected to achieve total savings of approximately £16,270.

Other non ESOS related actions which where documented proceeded to be completed for one of the stores is shown below. The ESOS action plan does not have to limited to recommendations identified within the audit.

Leveraging Professional Support & How Energy Technical Services Can Help

At ETS, we can support you with completing an action plan as well as, monitoring, verifying and reducing your energy use and hence your carbon emissions. We have the team and resources to audit your energy management systems to meet compliance standards. Some members of our team are ESOS certified and can quickly develop your net-zero strategy.

To discuss your requirements, get in touch. You can contact us by calling 0117 205 0542 or drop us an email at enquiries@energy-ts.com.

Ongoing Monitoring and Reporting: How businesses can continue to monitor their energy use and adapt their strategies for long-term sustainability

Businesses can sustain and enhance their energy efficiency efforts by continuously monitoring energy usage and adapting strategies over time. Regularly reviewing the timelines and milestones outlined in their action plan ensures consistent progress and alignment with objectives.

ETS provides an advanced energy management platform that enables participants to track their actions in compliance with IPMVP (International Performance Measurement. & Verification Protocol) standards. This platform ensures that implemented measures are monitored effectively and continue to deliver optimal performance and guaranteed savings from our energy managers over the long term.

Government Requirements for ESOS Phase 3

Key dates and requirements for completing energy audits and submitting reports:

Milestone | Dates |

Compliance period | 6 December 2019 to 5 December 2023 |

Action plan submission deadline | 05 December 2024 (<5 March 2025) |

Period covered by the action plan | 6 December 2023 to 5 December 2027 |

ESOS Progress update 1 deadline | 05 December 2025 |

Relevant reporting period to be covered by progress update 1 | 6 December 2024 to 5 December 2025 |

ESOS Progress update 2 deadline | 05 December 2026 |

Relevant reporting period to be covered by progress update 2 | 6 December 2025 to 5 December 2026 |

Regulatory Changes in Phase 3:

SN | ESOS Phase 3 / 4 Changes | Impact |

1 | Standardised template for including compliance information in ESOS report. | ETS will ensure our clients are compliant by adhering to new standards. |

2 | De-minimis rule has been reduced from 10% to 5%. | This means that the level of audit is wider reaching, and some previously omissible energy will need to be included. Proper Jobs are unlikely to be affected unduly. This is applicable to phase 3. |

3 | Intensity metrics should be included in the overview section of the reports. | ETS does this as standard and will be included in your report. |

4 | ESOS reports should provide more information on next steps for implementing recommendations. | Action plans will provide a better level of information for our clients to help them prioritise and act. |

5 | Identified opportunities should be shared with subsidiaries. | This means that parent entities or groups should share information to benefit the whole organisation. |

6 | Following phase 3, an improvement target or action plan must be defined and reported against in phase 4. | ETS produces this as standard, but this means that the organisation will be accountable for action plans moving forward although they are not enforced, suitable transparency and progression is expected. |

7 | There should be an annual report of target progress either through energy efficiency narrative from the company, SECR, or through ESOS public disclosure website | More transparency and effective reporting annually to ensure that organisations are accountable and progressing with improvements. |

8 | Additional data/information about the performance of participants in relation to energy management and behaviour change, and how this can be improved. This can be information regarding consumption change compared to previous phases, net-zero inclusion, energy management measures not implemented. | Awareness training and behaviour is an important aspect of energy management and drawing more of a focus that will benefit an organisation in saving energy through better engagement of the workforce. Auditors are expected to explore and comment on these aspects. |

9 | Sampling – minimum threshold for both the number of sites sampled and the percentage of total energy consumption sampled. These could be set differently for types or sizes of site, similarly to the way in which thresholds are set for air conditioning inspections. For example, for industrial sites and sites over 1000m2 the threshold could be 30% of energy consumption or a minimum of 4 sites (whichever is greater) and for non-industrial sites under 1000m2 the threshold could be 10% of energy consumption or a minimum of 4 sites. | In phase 4, prescriptive sampling and more explicit methodologies will be provided. This relates to clients with property portfolios and of facilities with varying applications and types. |

10 | No change to surveys |

Penalties for Non-Compliance

There is currently no fixed penalty or fine for noncompliance, however, the Environment Agency is authorized to issue a compliance notice (under Regulation 35(1)) or an enforcement notice (under Regulation 38) to mandate the submission of an action plan.

Non-compliance with these notices may result in financial penalties and the imposition of a publication penalty. The Environment Agency will decide on appropriate actions, if any, in line with its Enforcement and Sanctions Policy.

Creating an Effective Action Plan for Energy Savings

The Environment Agency has issued a template for the information required to submit an anion plan. This should include:

all the actions you intend to take to save energy, that you will carry out before end of the action plan period (which for action plans relating to the third compliance period is 5 December 2027)

for each action, the month and year you intend to take the action

for each action, whether it was recommended by an energy audit

for each action, an estimate of the total energy savings you will achieve during the action plan period through carrying out the action

for each estimate, the source of data used for the estimate

a combined estimate of the total energy savings you will achieve during the action period across all actions you will take

a breakdown of these savings by organisational purpose (buildings, transport, industrial processes and other energy use)

However, it is important to note that organisations should have:

A. An action plan that that includes specific timelines and milestones to monitor progress and maintain consistent implementation of energy-saving initiatives, that can be internally circulated to those required to complete the necessary actions. This ensures a regular progress update of the actions which needs to be reported annually. Develop a comprehensive action plan.

B. Evidence pack: This should include document of the methodology used to calculate the estimated and achieved savings.

The EA has advised that if a participants published action plan does not propose measures but subsequently but later implements measures to reduce energy consumption, the participant can still include those measures in your annual progress updates.

Prioritise energy-saving measures based on cost, impact, and feasibility

When deciding which energy-saving measures to implement, it is essential to evaluate them based on three key factors: cost, impact, and feasibility. A structured approach ensures that resources are allocated effectively to achieve the greatest benefits.

i. Cost

• Initial Investment: Assess the upfront costs of implementing the measure, including equipment, installation, and labour. Cost of actions are usually ranked:

o no cost (set-point and time schedule adjustment, switching off lights, closing doors, etc.);

o low cost measures (adding or improving controls etc.);

o high cost measures (building envelope, technical building equipment, etc. major technical system modifications, renewable energy, CHP, etc);

• Operational Costs: Consider any ongoing costs, such as maintenance or training.

• Payback Period: Calculate how long it will take for the savings generated to cover the initial investment. Prioritize measures with shorter payback periods if budget constraints exist. Often, energy efficiency improvement opportunities are commonly ranked using simple payback time. However, other financial metrics, such as return on investment (ROI) or net present value (NPV), can also be employed based on the client’s preferences.

• Return on Investment (ROI): Focus on measures that deliver the highest ROI over their lifetime.

ii. Impact:

• Savings: Evaluate the potential reduction in energy consumption and bills and how it aligns with the organization’s goals.

• Environmental Impact: Prioritize measures that significantly lower carbon emissions and contribute to sustainability targets.

• Operational Benefits: Consider non-financial impacts, such as improved comfort, health and well-being, productivity, or reliability of equipment.

iii. Feasibility:

• Technical Viability: Assess whether the measure is compatible with existing systems and infrastructure.

• Ease of Implementation: Determine how quickly and easily the measure can be implemented with minimal disruption.

• Regulatory Compliance: Consider whether the measure helps meet legal or policy requirements.

• Stakeholder Buy-In: Evaluate the willingness of employees, management, or other stakeholders to support the change.

• Scalability: Consider whether the measure can be expanded or adapted for future needs.

Prioritisation Strategy

Start with low-cost, high-impact measures that are easy to implement, such as switching to LED lighting or optimizing HVAC settings. Then medium-term investment projects with moderate costs and significant long-term savings, such as upgrading insulation or replacing outdated equipment can be considered. Finally, long-term goals like adopting renewable energy sources, which require more resources but offer substantial benefits over time can be implemented.

Financial and environmental benefits of committing to energy-saving initiatives

Lower Energy Bills: Reducing energy consumption leads to significant savings on utility costs, directly impacting the bottom line.

Reduction in Carbon Emissions: Energy-saving measures decrease greenhouse gas emissions, contributing to the fight against climate change.

Improved ROI: Investments in energy-efficient technologies and systems often deliver substantial returns over time through reduced operational costs.

Access to Incentives: Businesses may qualify for government grants, tax rebates, or other financial incentives for implementing energy-saving measures.

Increased Asset Value: Energy-efficient buildings and systems enhance property value and appeal to eco-conscious investors and tenants.

Corporate Social Responsibility (CSR): Demonstrating commitment to sustainability enhances reputation and builds trust with stakeholders, employees, and customers.

Reduced Maintenance Costs: Upgraded, energy-efficient equipment typically requires less maintenance and operates more reliably.

Enhanced Competitiveness: Cost savings free up capital for other investments, strengthening overall market competitiveness.

Improved Air and Water Quality: Decreased emissions from energy production lead to healthier ecosystems and communities.

Alignment with Net Zero Goals: Adopting energy-saving measures helps organizations align with national and global sustainability targets.

Support for Renewable Energy: Reduced energy consumption complements the transition to renewable energy systems by reducing overall demand.

Related Article

8 Ways Businesses Can Reduce Energy Use in the Workplace This Winter

Discover how to comply with ESOS Phase 4 and unlock energy-saving opportunities for your business. This guide explains the requirements, highlights key deadlines, and provides actionable strategies. Learn how energy audits, tailored action plans, and expert support can reduce costs, improve efficiency, and align your organisation with sustainability goals.

Important Update: What You Need to Know about ESOS Phase 3

Time is ticking for the ESOS Phase 3 deadline. The Environment Agency announced that the reporting system is available now. For organisations qualifying for ESOS Phase 3, the deadline for submitting a compliance notification is 5 June 2024, and organisations should still look to meet this compliance notification deadline where possible.

Earth Day 2024

Earth Day represents a vital reminder of our planet’s fragility and the importance of preserving its natural resources for future generations. It’s a time to unite to combat climate change, protect ecosystems, and promote environmental stewardship.